Many producers have increasingly turned to using options in their margin management plans over the past several years. I think there have been several factors that have contributed to this trend. First, there has been quite a bit of volatility in both profit margins across the various livestock and crop industries, as well as the prices of the individual commodities that comprise the costs and revenues of those industries. We have seen record high prices in many of these commodities recently, including corn, wheat, soybeans, cattle, milk and hogs. We have also witnessed significant price moves both up and down in each of these commodities. Options provide price protection while offering opportunity. With greater fluctuation in price, the opportunity cost of simply fixing a price level as opposed to protecting a price level increases. Second, I think there has been an increased level of understanding in how options work and the effective use of these tools to protect price levels and profit margins. While there is still quite a bit of education that is needed to help agricultural producers feel more comfortable using these strategies in their margin management plans, we have certainly seen more adaption of options into producers’ toolbox over time.

A common objection to using options however remains the cost of the premium paid for maintaining the flexibility that they provide. It is certainly true that options carry a cost, and this cost can be substantial depending on many factors including how much time is remaining to the option’s expiration and how volatile the underlying price of the commodity has been. One way to measure the relative cost of an option is to consider its implied volatility. This is calculated by taking the option’s premium and plugging it into a model with other inputs such as the time to expiration, interest rates, the option’s strike price, and volatility of the underlying futures contract upon which the option is priced. The resulting value of implied volatility can then be used to measure the nominal premium of the option within an objective context so that it can be evaluated effectively. As a general note, the nominal premium of an option can rise simply as a function of an increase in price in the underlying commodity. As an example, if corn is trading at $7.00/bushel, the nominal premium of options to protect a purchase or sale price at that level is going to be higher than if corn is trading at $3.50/bushel, simply as a function of corn being twice as expensive. This does not necessarily mean that the implied volatility of those options is higher however.

Implied volatility has to do with the market’s perception of how volatile the underlying commodity’s price will be in a future time period. If in the previous example, there is widespread uncertainty as to whether corn is trading at the $7.00 price level on its way to $10.00, or if the price is primed for a crash back down to $4.00, this is very different than a perception that corn is going to stay around the $7.00 price level plus or minus $1.00 relative to the dynamics in play at that point in time. In the present environment, corn has experienced a significant drop in price over the past few months. The main fundamental factor contributing to this decline is the expectation of a record-large crop to be harvested this fall with production exceeding total demand for the first time since the 2009-10 marketing year. The resulting increase in total corn stocks both in absolute terms as well as in relation to total usage is expected to keep a lid on prices and act as an impediment to any rally attempt over the medium-term. At the same time though, lower prices have boosted margins for a number of industries including livestock feeding and ethanol production. Lower corn prices will also make exports more attractive to foreign buyers, although the U.S. dollar has recently been showing strength. Increased demand will offer support to corn prices which will probably begin to temper further losses following the significant drop in price we have already experienced.

Given parallel expectations for limited upside potential and limited further downside pressure, the market’s collective expectation for corn prices has become one of a compressed range which can be thought of in terms of reduced volatility moving forward for a significant move in either direction. Whether or not this expectation plays out with actual price action in the weeks and months ahead, the result is lower option premiums across all strike prices for several months forward in time. What does this mean from a hedger’s perspective in trying to manage forward margins? Consider the crop producer on the one hand. Here, margins are depressed and actually negative for both the current crop in the ground as well as the 2015 production. The obvious choice here would be to use a flexible strategy in order to preserve the opportunity for a positive margin over time. Therefore, an option position would make sense for a crop producer given their current projected profit margins. Now consider the livestock or ethanol producer. Here, the margin may not only be positive, but may actually be very strong from a historical perspective. The inclination would be to “lock-in” the projected strong margin opportunity, although the implied volatility is suggesting otherwise.

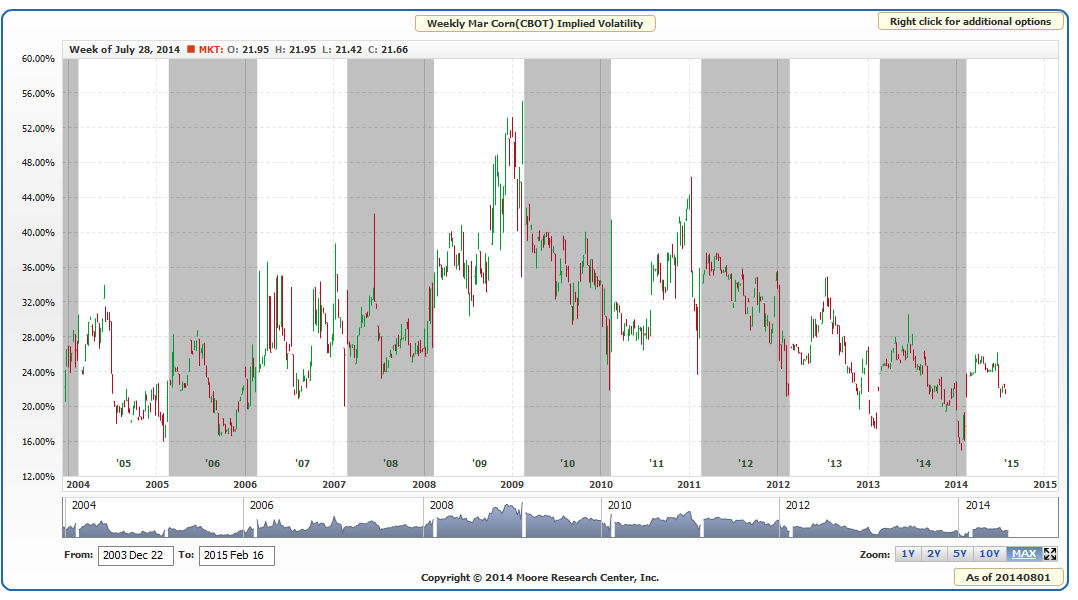

One way of thinking about options in a low volatility environment is that the premium is depressed in relative terms and therefore “on sale.” The following chart shows the implied volatility of March 2015 Corn options:

The chart plots where implied volatility for the March Corn options has traded relative to where it is currently priced today. Current implied volatility is trading around 21%-22%. From a historical perspective, implied volatility under 20% is cheap when looking at the chart going back 10 years to 2004 while implied volatility over 40% would be considered expensive. When you purchase an option, you own a right to a purchase or sale price of the underlying commodity at a certain level over a period of time. In other words, you own an asset that is depreciating as a function of time decay and how close the option is to expiration. In a low volatility environment (such as we have today with corn), you are purchasing a deflated asset in that expectations are muted for a significant price move over a period of time. In a high volatility environment by contrast, you would be purchasing an inflated asset where the loss of premium through time decay may become more pronounced if volatility begins to contract.

Getting back to the livestock or ethanol producer and managing forward profit margins in those industries, it may be better to use flexible strategies to protect margins given the low implied volatility of options because the premium is attractively valued or priced. Ideally, the margin improves over time where the flexibility can be traded out for a fixed price commitment, but incorporating more flexibility into margin management strategies can be a distinct benefit in a low implied volatility environment. While the choice of using one strategy alternative over another will come down to the individual preferences of different operations and their unique considerations and risk profiles, the current low implied volatility of corn and other commodities for that matter should not be overlooked when evaluating various strategies that can be used to manage forward profit margins.